當地時間8月26日,美聯儲主席鮑威爾在全球矚目的傑克遜霍爾央行年會上,發表了個人認為是年度最“鷹”的一次講話,甚於6、7月例會,美股聞訊大幅回撤。

鮑威爾認為,當前的主要矛盾仍是通脹,他首先是擔心“緊縮不足”,其次才是“過度緊縮”。 這次會議中提到的「三個教訓」,一是向市場傳遞信心,美聯儲可以實現低且穩定的2%通脹目標; 二是強調通脹預期發揮的「錨」的作用,聯繫到了工資-物價螺旋,因為勞動力市場依然非常緊張; 三是明確了“緊縮不足”的風險。 如果市場領會了鮑威爾的意思,長期通脹預期會進一步下行,或至少會保持在略高於2%目標的水準上,而不會脫錨。

以下是鮑威爾講話的全文、翻譯和筆者的評議。

1. Thank you for the opportunity to speak here today.

謝謝給我今天在這裡演講的機會。

2. At past Jackson Hole conferences, I have discussed broad topics such as the ever-changing structure of the economy and the challenges of conducting monetary policy under high uncertainty. Today, my remarks will be shorter, my focus narrower, and my message more direct.

在以前的傑克遜霍爾會議上,我討論的話題很廣泛,比如不斷變化的經濟結構,以及在高度不確定的環境中實施貨幣政策的挑戰。 今天,我的講話將會更簡短,重點更集中,資訊更直接。

3. The Federal Open Market Committee's (FOMC) overarching focus right now is to bring inflation back down to our 2 percent goal. Price stability is the responsibility of the Federal Reserve and serves as the bedrock of our economy. Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all. The burdens of high inflation fall heaviest on those who are least able to bear them.

聯邦公開市場委員會(FOMC)目前的首要任務是將通脹降到2%的目標水準。 物價穩定是美聯儲的職責所在(注:寫進了《聯邦儲備法案》),也是我們經濟平穩運行的基石。 沒有價格穩定,經濟的運行對任何人來說都將是不合意的。 特別是,如果沒有價格穩定,我們將無法恢復有利於所有人的、持久的和強勁的工作力市場。 高通脹最沉重的負擔將會落在那些最無力承受的人的身上。

評議:美聯儲的貨幣政策現在非常關注分配與公平。

20世紀70年代中期以來,美國貧富分化問題日漸突出。 這在收入流量與財富存量分配格局中都有體現。 一般認為,其原因主要是結構性的——技能偏好性技術進步、經濟的全球化和金融化、市場集中度和企業議價能力的提升、數字經濟的“贏家通吃”特徵等。 長期以來,美聯儲貨幣政策目標並未明確包含分配的維度,但越來越多的證據顯示,分配格局的惡化卻直接影響到“物價穩定”和“最大就業”目標的實現,因為貧富分化是導致經濟長期停滯、壓抑自然利率和物價水準的重要原因。 所以,如何更好地調節收入分配已經成為美聯儲貨幣政策的題中之意。 2008年大危機以來,量化寬鬆政策在托底整體經濟和阻遏風險傳染的同時,也會通過資產價格重估效應而加劇財富分配的不均等,這又反過來影響到經濟復甦的持續性,提高貨幣政策面臨“零利率下線”約束的長期性。 所以,美聯儲必須考慮貨幣政策的分配效應。 疫情衝擊的特殊性在於,大量就業者退出了勞動力隊伍,勞動參與率大幅下挫,這使得官方失業率顯著低估了真實失業水準和失業缺口。 後疫情時代,被低估的失業率和就業市場的“K型復甦”特徵成為美聯儲退出非常規政策的“絆腳石”。

4. Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.

恢復價格穩定還需要一段時間,這需要我們有力地運用貨幣政策工具,使需求和供應更好地平衡。 為了降低通脹,經濟增長速度可能在一段時間內會持續低於潛在增速。 而且,勞動力市場狀況很可能會有所弱化。 利率的上升、經濟增長速度的放緩和就業市場的疲軟都會降低通脹,但也會給家庭和企業帶來一些痛苦。 這些都是降低通脹不幸的代價。 如果不能實現價格穩定,損失會更嚴重。

評議:供不應求是當前通脹的成因,貨幣政策只能作用於需求,故只能通過收縮需求壓制通脹。 鮑威爾接受了壓制通脹會犧牲短期經濟增長的事實,但強調這是“兩害相權取其輕”,算是在為後文做鋪墊。

5. The U.S. economy is clearly slowing from the historically high growth rates of 2021, which reflected the reopening of the economy following the pandemic recession. While the latest economic data have been mixed, in my view our economy continues to show strong underlying momentum. The labor market is particularly strong, but it is clearly out of balance, with demand for workers substantially exceeding the supply of available workers. Inflation is running well above 2 percent, and high inflation has continued to spread through the economy. While the lower inflation readings for July are welcome, a single month's improvement falls far short of what the Committee will need to see before we are confident that inflation is moving down.

相對於2021年歷史最高水平的經濟增速而言——反映了大流行衝擊后的經濟重啟,美國經濟增長率開始明顯放緩。 雖然最新的經濟數據好壞參半,但在我看來,我們的經濟繼續保持著強勁的動能。 勞動力市場尤其強勁,但它顯然是失衡的,對工人的需求大大超過了可用工人的供應。 通貨膨脹率遠高於2%,高通貨膨脹率繼續在經濟中蔓延。 儘管7月通脹數據下降了,這令人欣慰,但單個月的下降還遠不足以使委員會確信通脹的拐點已經出現。

評議:如何才能讓FOMC確信通脹的拐點已經確立了? 這是分析的要點,顯然,7月單月的小幅下行是不滿足條件的。 個人認為,既要關注通脹的水準,也要關注結構、動態的路徑和波動率。

6. We are moving our policy stance purposefully to a level that will be sufficiently restrictive to return inflation to 2 percent. At our most recent meeting in July, the FOMC raised the target range for the federal funds rate to 2.25 to 2.5 percent, which is in the Summary of Economic Projection's (SEP) range of estimates of where the federal funds rate is projected to settle in the longer run. In current circumstances, with inflation running far above 2 percent and the labor market extremely tight, estimates of longer-run neutral are not a place to stop or pause.

我們會確保一個足夠緊縮的政策立場,以使通貨膨脹下降到2%的水準。 在7月的會議上,FOMC將聯邦基金利率的目標區間上調至2.25 - 2.5%,這是經濟預測摘要(SEP)對長期聯邦基金利率區間的估計(注:即中性利率區間)。 目前的特徵事實是,通脹遠高於2%,且就業市場極度緊張。 所以,還不是停止或暫停加息的時候。

評議: 加息表明貨幣政策趨於收緊,但不一定是過緊(或偏緊),只要FFR低於中性利率,就可以認為貨幣政策還處於寬鬆區間。 可將FOMC季度預測(SEP)當中關於FFR的長期預測視為中性利率,2022年6月的最新預測為2.5%,等於7月加息後FFR目標區間的上限。 這意味著,9月加息後,貨幣政策才從偏鬆轉向偏緊。 疫情之後,數據雜訊較大,一個較為普遍的觀點認為,對中性利率的估計存在較大的誤差,以至於紐約聯儲都暫停對外發佈模型的最新預測結果。 實踐中,可用美國國債期限結構來衡量貨幣政策的鬆緊程度,常用的指標有:3個月國庫券與10年國債的期限利差(3M-10Y)、1年國債與10年國債利差(1Y-10Y)或2年國債與10年國債利差(2Y-10Y)。 三個指標的走勢基本一致。 3M-10Y與另外兩個指標短期可能出現背離,但遲早會收斂。

7. July's increase in the target range was the second 75 basis point increase in as many meetings, and I said then that another unusually large increase could be appropriate at our next meeting. We are now about halfway through the intermeeting period. Our decision at the September meeting will depend on the totality of the incoming data and the evolving outlook. At some point, as the stance of monetary policy tightens further, it likely will become appropriate to slow the pace of increases.

7月是今年第二次加息75個基點,我當時說,再來一次不同尋常的大幅度的加息可能是合適的。 我們現在大約已經過了休會期的一半。 9月例會的決定將取決於獲得的全部數據和不斷演變的前景。 在某個時點,隨著貨幣政策的立場進一步收緊,放緩加息的步伐可能是合適的。

評議:“ 某個時點“的確定主要取決於美聯儲是否確認通脹正在確定地朝著2%目標收斂。 美聯儲內部的研究人員一般會給一個預測的通脹路徑,FOMC成員會結合就業等基本面信息的預測,反推不同時點合適的貨幣政策立場。 當然,后疫情時代預測非常不靠譜,FOMC也必須將這一點考慮進來。

8. Restoring price stability will likely require maintaining a restrictive policy stance for some time. The historical record cautions strongly against prematurely loosening policy. Committee participants' most recent individual projections from the June SEP showed the median federal funds rate running slightly below 4 percent through the end of 2023. Participants will update their projections at the September meeting.

恢復物價穩定可能(還)需要在一段時間內保持緊縮的政策立場。 歷史的經驗教訓對過早地放鬆政策提出了強烈警告。 6月的SEP顯示,FOMC成員預測到2023年底聯邦基金利率的中位數略低於4%。 FOMC將在9月的會議上更新他們的預測。

評議:正如我在點評7月會議紀要中說的,美聯儲首先是擔心緊縮不足,其次才是緊縮過度。

9. Our monetary policy deliberations and decisions build on what we have learned about inflation dynamics both from the high and volatile inflation of the 1970s and 1980s, and from the low and stable inflation of the past quarter-century. In particular, we are drawing on three important lessons.

我們對貨幣政策的審議和決策基於我們從上世紀七八十年代的高且不穩定的通脹以及過去四分之一世紀的低而穩定的通脹中對通脹的認識。 值得強調的是,我們吸取了三個重要教訓:

10. The first lesson is that central banks can and should take responsibility for delivering low and stable inflation. It may seem strange now that central bankers and others once needed convincing on these two fronts, but as former Chairman Ben Bernanke has shown, both propositions were widely questioned during the Great Inflation period.1 Today, we regard these questions as settled. Our responsibility to deliver price stability is unconditional. It is true that the current high inflation is a global phenomenon, and that many economies around the world face inflation as high or higher than seen here in the United States. It is also true, in my view, that the current high inflation in the United States is the product of strong demand and constrained supply, and that the Fed's tools work principally on aggregate demand. None of this diminishes the Federal Reserve's responsibility to carry out our assigned task of achieving price stability. There is clearly a job to do in moderating demand to better align with supply. We are committed to doing that job.

第一個教訓是,央行能夠且應該承擔起實現低而穩定的通脹的責任。 回看歷史,以前還需要說服中央銀行家們和其他人接受這兩點似乎有些奇怪,但正如前主席本·伯南克所表明的那樣,這兩個主張在大通脹時期都受到了廣泛的質疑。 今天,這些問題已經解決了。 維護價格穩定,我們責無旁貸。 的確,目前的高通脹是一個全球現象,許多經濟體都面臨著高通脹壓力,有的國家甚至比美國還要高。 在我看來,美國目前的高通脹也是強勁的需求和受限的供給共同的結果。 美聯儲的工具主要針對總需求。 但這不會削弱美聯儲承擔維護價格穩定任務的責任。 顯然,我們需要做的是緩和需求,使其與供應更好地匹配。 我們正致力於此。

評議:對外安撫市場、公眾,對內建立自信,給小夥伴們打氣。

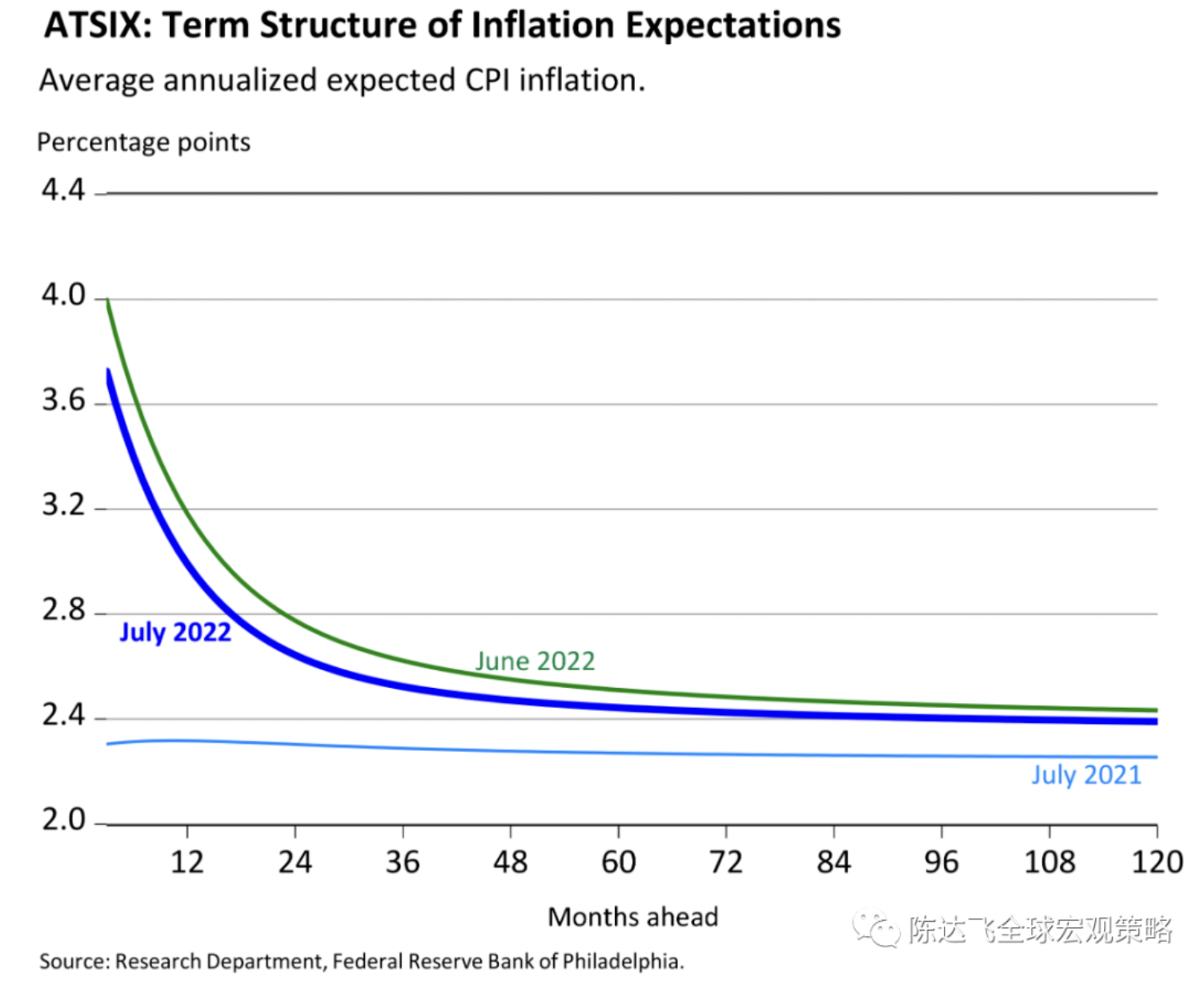

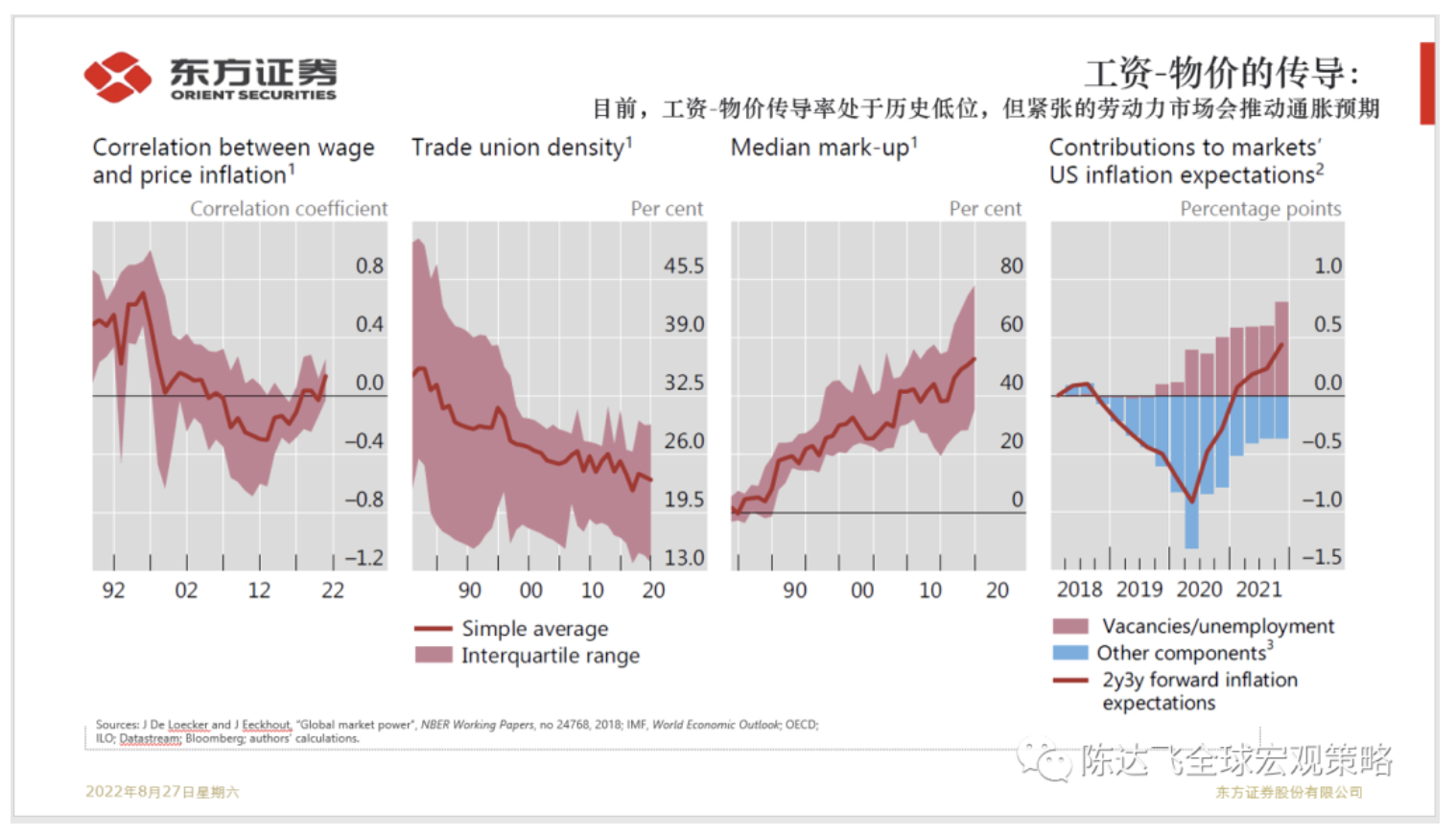

11. The second lesson is that the public's expectations about future inflation can play an important role in setting the path of inflation over time. Today, by many measures, longer-term inflation expectations appear to remain well anchored. That is broadly true of surveys of households, businesses, and forecasters, and of market-based measures as well. But that is not grounds for complacency, with inflation having run well above our goal for some time.

第二個教訓是,公眾對未來通脹的預期可以在通脹的未來走向方面發揮重要作用。 當下,從許多指標來看,長期通脹預期的“錨”還在。 對家庭、企業和預測機構的調查,以及基於市場的衡量標準,大致都是如此。 但這不是自滿的理由,通脹遠高於我們的目標已經有一段時間了。

評議:通脹預期在持續高通脹的形成過程中至關重要。 當前,美國的短期通脹預期明顯高於長期——通脹的期限結構是倒掛的,這是美聯儲還能夠在一定程度上去平衡短期與長期目標的原因。 穩定的通脹預期能為貨幣政策當局提供更多跨期最優決策的空間,即不以短期目標而犧牲中長期目標。 相反,通脹預期越不穩定,錨定通脹預期的成本就越高,也就越要求貨幣當局對短期的壓力做出更積極的回應,而這可能要求犧牲長期目標。

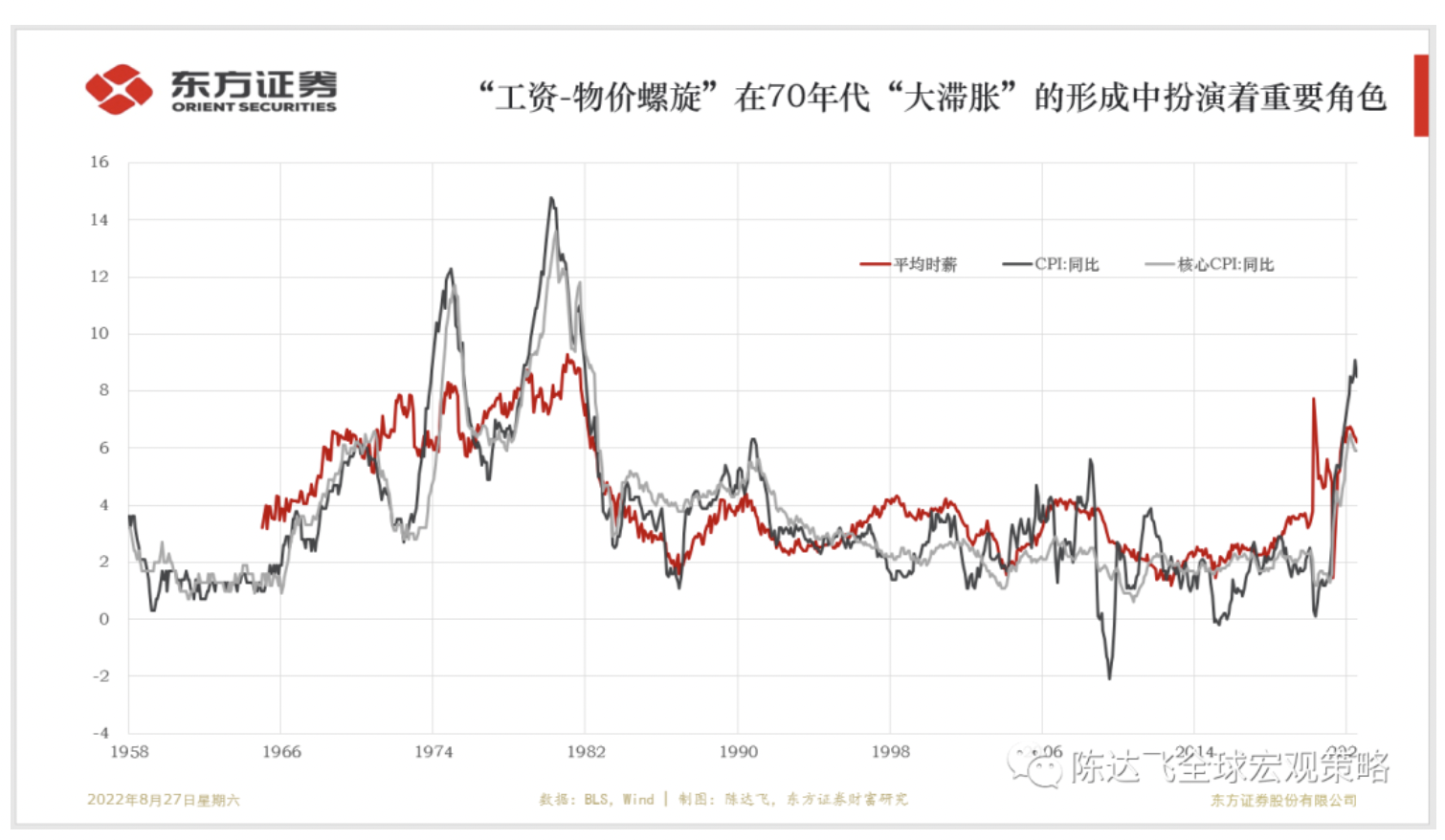

12. If the public expects that inflation will remain low and stable over time, then, absent major shocks, it likely will. Unfortunately, the same is true of expectations of high and volatile inflation. During the 1970s, as inflation climbed, the anticipation of high inflation became entrenched in the economic decision-making of households and businesses. The more inflation rose, the more people came to expect it to remain high, and they built that belief into wage and pricing decisions. As former Chairman Paul Volcker put it at the height of the Great Inflation in 1979, "Inflation feeds in part on itself, so part of the job of returning to a more stable and more productive economy must be to break the grip of inflationary expectations."

如果公眾預期通脹將在一段時間內保持在低且穩定的水準上,那麼,在沒有重大衝擊的情況下,實際情況很可能也會如此。 不幸的是,對於高且不穩定的通脹預期也會自我實現。 上世紀70年代,隨著通脹的攀升,對高通脹的預期在家庭和企業的經濟決策中變得根深蒂固。 通貨膨脹率越高,人們就越預期它還會保持在高位,他們把這種信念嵌入在工資和定價決策上。 正如前美聯儲主席保羅•沃爾克在1979年通脹達到頂峰時說的,“通脹在一定程度上是自我反饋的,因此,要想恢復一個更穩定、生產率更高的經濟,必須將一部分精力放在控制通脹預期上。 ”

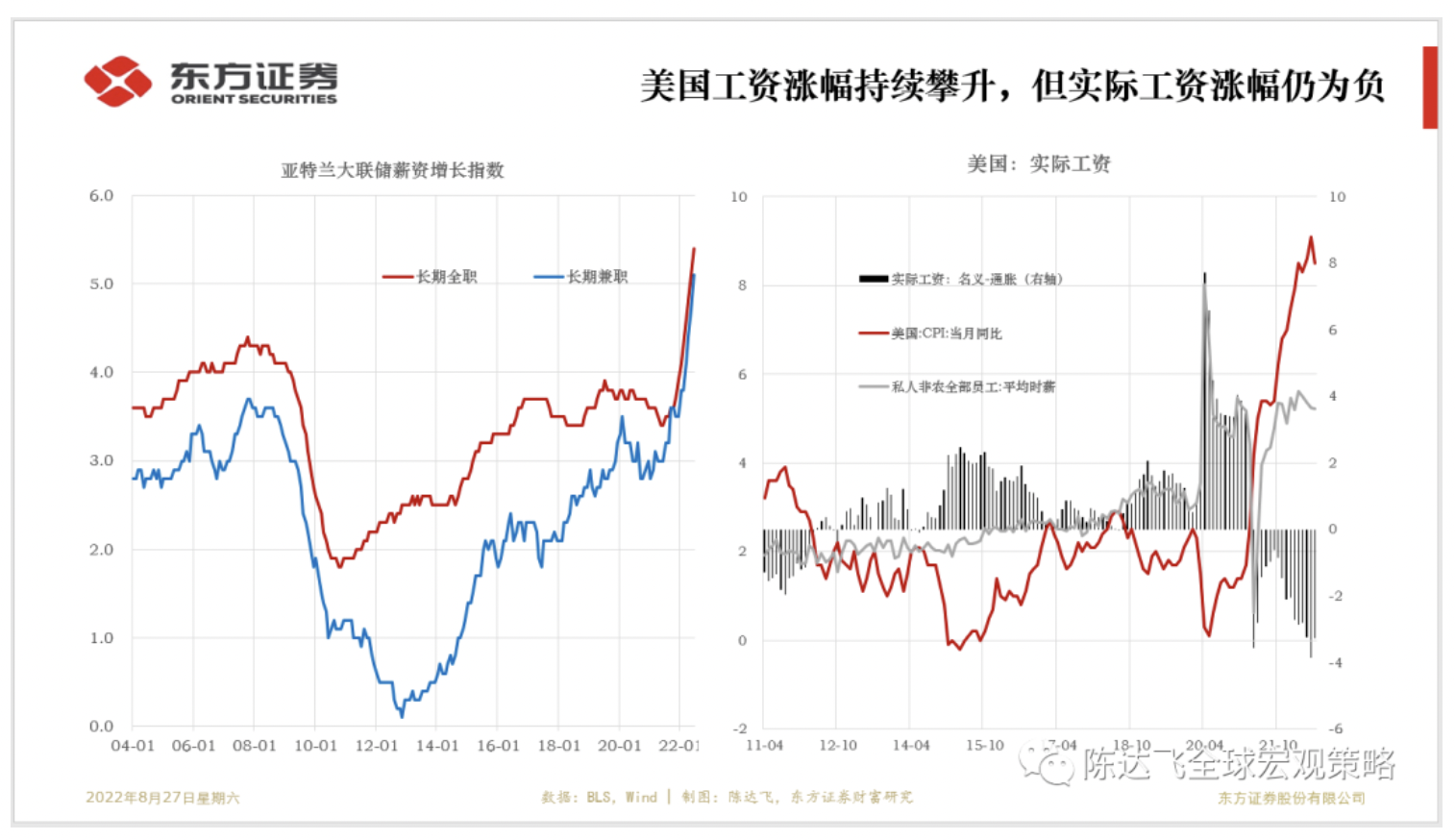

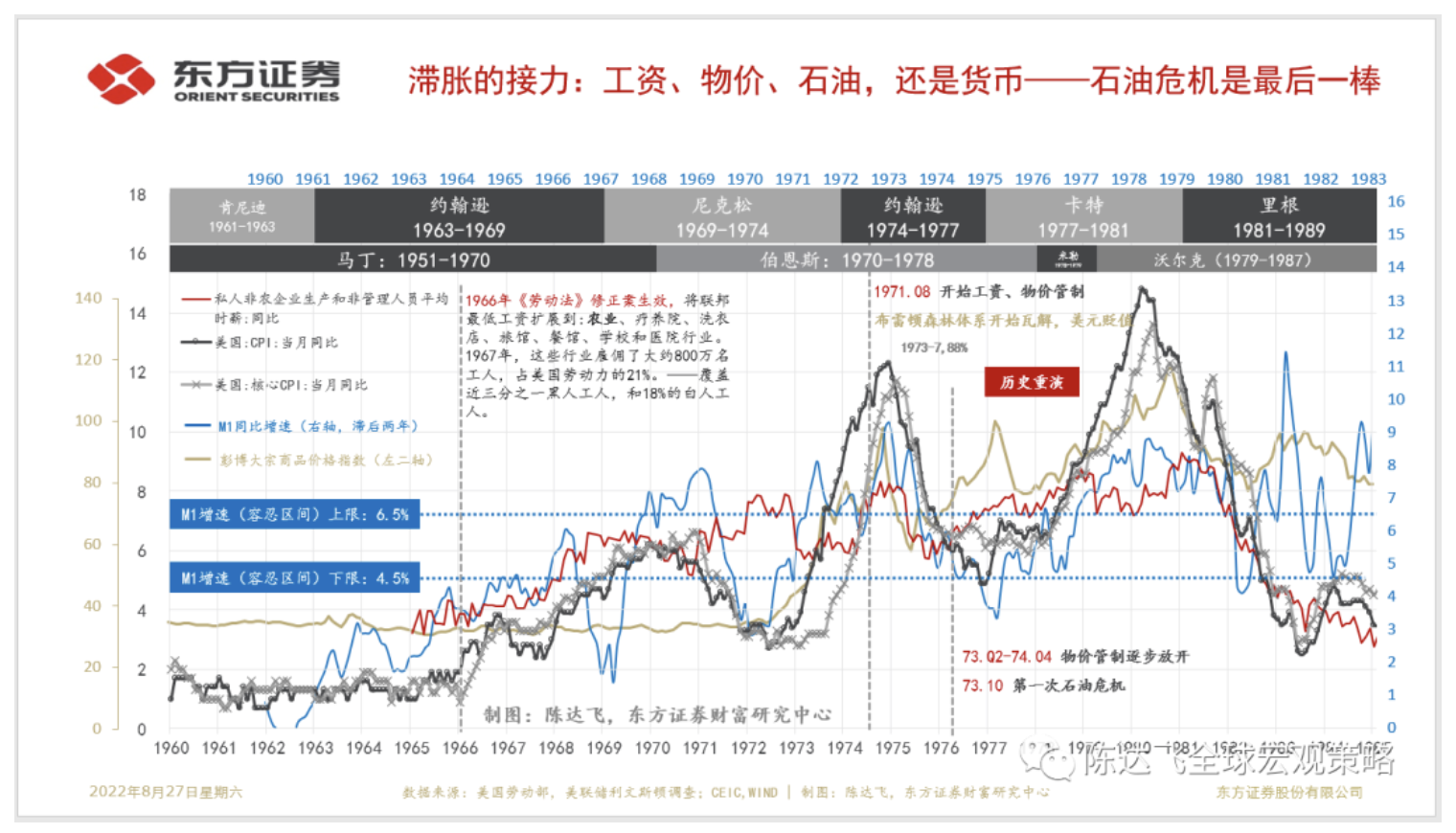

評議:通脹預期會自我實現。 貨幣當局之所以關注通脹預期,原因是它對定價行為的影響,包括物價和工資,以及二者之間的正反饋關係。 當預期通脹居高不下時,勞動者一般會要求更高的工資,或指數化的工資決定機制,比如與生活成本(Cost-of-Living Adjustment,COLA)挂鉤。 當企業預期到要素成本存在上行壓力時,會根據議價能力和商品的需求價格彈性的大小選擇將一部分成本轉嫁給消費者,從而形成“工資-物價螺旋”。 這是20世紀70年代「大滯脹」形成的重要原因。 工資決定的是通脹的趨勢,而非波動。 “工資-物價螺旋”一旦形成,通脹預期就脫錨了。 是貨幣當局最不願意面對的環境。 工資和物價都是有粘性的,「工資-物價螺旋」的形成有較高的前置條件,比如緊張的工作力市場、較高的集體談判權、寬鬆的貨幣政策、較高的中長期通脹預期等。 “大緩和”時代以來,市場和政策制定者都習慣了通脹預期穩定或存在通脹缺口的宏觀環境,忘卻了“工資-通脹螺旋”的風險。 直到2022年7月例會,FOMC依然否認“工資-通脹螺旋”是通脹的一個成因,當然這也是市場的共識,但不可否認風險正在積聚。

13. One useful insight into how actual inflation may affect expectations about its future path is based in the concept of "rational inattention." 3 When inflation is persistently high, households and businesses must pay close attention and incorporate inflation into their economic decisions. When inflation is low and stable, they are freer to focus their attention elsewhere. Former Chairman Alan Greenspan put it this way: "For all practical purposes, price stability means that expected changes in the average price level are small enough and gradual enough that they do not materially enter business and household financial decisions." 4

關於實際通脹可能會怎樣影響人們對其未來走向的預期,一個有用的洞見建立在“理性忽視”的概念上。 當通貨膨脹持續高企時,家庭和企業必須密切關注並將通貨膨脹納入他們的經濟決策。 當通貨膨脹處於低位且穩定時,他們可以更自由地將注意力集中在其他地方。 前美聯儲主席艾倫·格林斯潘這樣說:“從實際角度來看,價格穩定意味著平均價格水平的預期變化足夠地小,足夠地平滑,它們不會實質性地影響企業和家庭的金融決策。”

評議:所謂「理性忽視」,就是注意不到通脹的存在,不將其納入到金融、經濟決策行為中,例如:不要求債權人不好求更高的通脹補償收益率,勞動者不要求更高的工資、企業不指定更高的物價等。

14. Of course, inflation has just about everyone's attention right now, which highlights a particular risk today: The longer the current bout of high inflation continues, the greater the chance that expectations of higher inflation will become entrenched.

當然,目前幾乎所有人都在關注通脹,這凸顯了一種特殊的風險:高通脹持續的時間越長,對通脹上升的預期變得更加根深蒂固的可能性就越大。

15. That brings me to the third lesson, which is that we must keep at it until the job is done. History shows that the employment costs of bringing down inflation are likely to increase with delay, as high inflation becomes more entrenched in wage and price setting. The successful Volcker disinflation in the early 1980s followed multiple failed attempts to lower inflation over the previous 15 years. A lengthy period of very restrictive monetary policy was ultimately needed to stem the high inflation and start the process of getting inflation down to the low and stable levels that were the norm until the spring of last year. Our aim is to avoid that outcome by acting with resolve now.

這就引出了我的第三個教訓,那就是我們必須堅持下去,直到工作完成。 歷史表明,隨著高通脹在工資和物價的制定中變得更加根深蒂固,降低通脹的就業成本可能會隨著時間的延遲增加。 上世紀80年代初沃爾克抗通脹的成功是在此前15年多次降低通脹的嘗試失敗之後發生的。 為了遏制高通脹,需要長期執行非常緊縮的貨幣政策,以將通脹降至低而穩定的水準——這是2021年春天之前的常態。 我們的目標是通過現在果斷的行動來避免這樣的結果(長期實施緊縮政策)。

評議:堅定信心,謹防在通脹剛剛有點下降的苗頭,或者下行的趨勢還不穩固的時候就理解轉變緊縮的政策立場,以權衡就業/經濟增長目標。

16. These lessons are guiding us as we use our tools to bring inflation down. We are taking forceful and rapid steps to moderate demand so that it comes into better alignment with supply, and to keep inflation expectations anchored. We will keep at it until we are confident the job is done.

這些經驗教訓在指導我們使用我們的工具來降低通貨膨脹。 我們正在採取有力而迅速的措施來調節需求,使其更好地與供給保持一致,並穩定通脹預期。 我們將繼續努力,直到我們確信完成了這項工作。

(文章僅代表作者觀點。 責編郵箱:yanguihua@Jiemian.com。 )

責任編輯:陳悠然